Nvidia Headlines Final Stretch of Earnings Season With AI Spending in Focus

More than 85% of S&P 500 companies have reported results, with profit growth expectations rising to 13.6% year-over-year. Nvidia, Salesforce and Home Depot headline a pivotal week for markets.

Daniel Brooks

Daniel Brooks

More than 85% of companies in the S&P 500 have now reported fourth-quarter results, bringing earnings season close to completion. According to FactSet, projected Q4 profit growth stands at 13.6% year-over-year, up from 8.1% at the start of the quarter.

Once again, investors are recalibrating expectations as corporate guidance and macro signals send mixed messages.

Sector Highlights: Strong Results, Cautious Reactions

Last week saw divergent performance across key sectors.

- Consumer: Walmart delivered solid results, but shares declined as management issued cautious forward guidance.

- Technology: Palo Alto Networks raised its annual revenue outlook amid strong demand. However, higher operating costs pressured the stock. Guidance improved. Margins didn’t.

- Industrials: Deere posted strong earnings and upgraded its outlook, supporting gains in the stock.

Market reaction suggests investors are increasingly sensitive not just to revenue beats, but to expense trends and capital allocation signals.

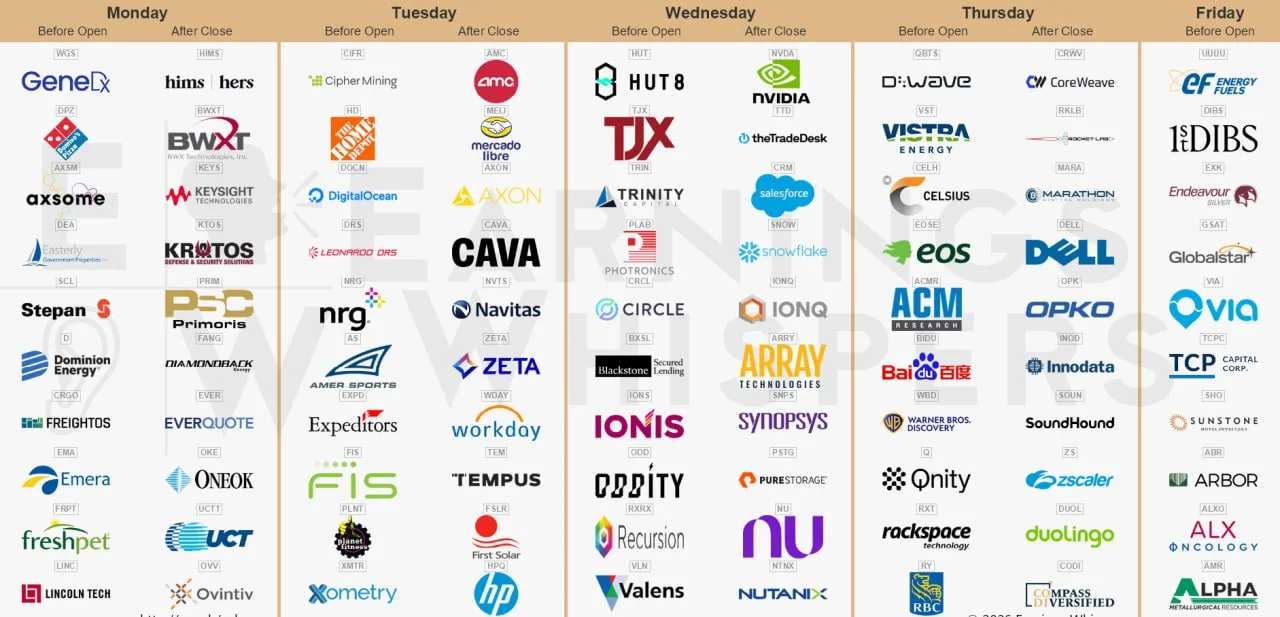

Key Earnings to Watch This Week

A total of 1,686 companies are scheduled to report this week, including 54 constituents of the S&P 500.

The most anticipated release comes from Nvidia (Feb. 25, after market close). As the largest company globally by market capitalization and a central force in the AI ecosystem, Nvidia’s results may define near-term sentiment across the technology sector.

The company reports amid rising scrutiny over Big Tech capital expenditures and potential investments of up to $30 billion in OpenAI. Investors will closely watch commentary from CEO Jensen Huang regarding AI chip demand and potential updates on access to the Chinese market.

Other notable names include Salesforce, Home Depot, Lowe’s, HSBC Holdings, Royal Bank of Canada, Intuit and MercadoLibre.

Macro Catalysts: Trump, Fed and Inflation Data

On February 24, U.S. President Donald Trump is scheduled to deliver a State of the Union address. Markets will be listening for commentary on tariffs, taxation and economic support measures.

Several senior officials from the Federal Reserve are also expected to speak, potentially shaping rate expectations.

- Feb. 25: S&P Case-Shiller Home Price Index (December)

- Feb. 27: U.S. Producer Price Index (January). Headline inflation is expected at 2.9% YoY, down from 3.0%, with core PPI projected at 3.3%.

- Feb. 25: Final January CPI for the Eurozone, with headline inflation projected at 1.7%.

With earnings season nearing completion, the market narrative is shifting from backward-looking results to forward guidance and macro risks. Nvidia’s report may serve as the next major catalyst.

Clean beat? Or cautious tone? Investors will be watching closely.

-

Li Auto Cuts Forecast as Price War Weighs on MarginsEarnings

Li Auto Cuts Forecast as Price War Weighs on MarginsEarnings -

Earnings Season Kicks Off as TSMC and Big Banks Set the Market ToneEarnings

-

Earnings Week Ahead: Alphabet, Amazon, AMD, Disney and 120+ S&P 500 ReportsEarnings

-

Q4 2025 Earnings Season Begins With Focus on US BanksEarnings

-

U.S. Earnings Season Gains Momentum as Profit Growth Outlook ImprovesEarnings

-

U.S. Earnings Season Accelerates as Investors Eye Tech and Financial ResultsEarnings