Why Investors Are Overpaying for Downside Protection While Shorting VIX

Nasdaq put-call skew remains elevated despite heavy short positioning in VIX futures. The apparent contradiction reflects different investor groups with different strategies — and could matter in the next downturn.

Olivia Carter

Olivia Carter

From a market-structure perspective, the current setup looks contradictory at first glance — but it isn’t.

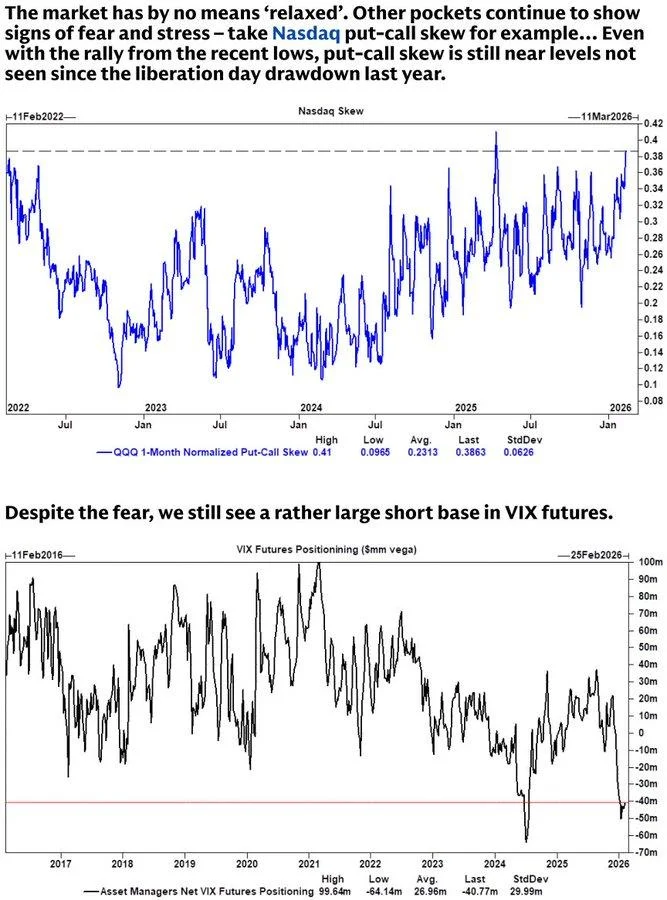

Nasdaq put-call skew remains elevated, signalling persistent demand for downside protection. Even after the recent rally, skew levels are hovering near extremes last seen during last year’s major drawdown. In simple terms: investors are still paying up for insurance.

At the same time, positioning data in VIX futures shows a rather large net short base among asset managers. That suggests many participants are effectively betting that realised volatility will remain contained.

Why This Isn’t a Contradiction

The key lies in understanding that these are two different markets with two different participant groups.

Institutional portfolio managers — pension funds, large asset allocators, multi-asset managers — typically hedge via direct put options on equities and indices. Their objective isn’t to trade volatility itself. It’s to protect portfolio drawdowns. When risk feels asymmetric, they buy protection regardless of cost.

This persistent demand pushes put premiums higher and steepens skew.

Meanwhile, volatility traders and macro funds operate in a different framework. Selling VIX futures can be a carry strategy, especially when realised volatility remains subdued. If daily moves are small and macro data stable, short volatility positions generate yield.

In other words: one group buys fire insurance. Another sells weather forecasts.

Different Motives, Different Risk Profiles

Buying puts is defensive and portfolio-specific. Shorting VIX futures is tactical and volatility-focused. The two strategies are not mechanically linked.

What matters is timing.

The real tension would emerge if markets start to decline sharply. In that scenario:

- Put buyers would be vindicated — but may seek additional protection.

- Short VIX positions could face forced covering.

- Liquidity conditions could tighten quickly.

That is when positioning alignment matters — when everyone suddenly wants the same hedge at the same time.

What It Signals Now

Elevated skew tells us large portfolios remain cautious beneath the surface of the rally. Heavy short VIX positioning tells us volatility sellers still see carry opportunities.

Markets can sustain this split positioning for months. They often do.

But structurally, it creates fragility. Not today — perhaps not tomorrow — yet the setup suggests that if a genuine downside catalyst appears, volatility could reprice faster than many expect.

Markets are rarely “relaxed” when protection stays expensive.

-

BofA Survey Signals Extreme Optimism as Cash Levels Hit Record LowsStocks

BofA Survey Signals Extreme Optimism as Cash Levels Hit Record LowsStocks -

News Flow Tilts the Balance Toward BuyersStocks

-

S&P 500 and Nasdaq Futures Consolidate Near Record Highs as Volatility Stays SubduedStocks

-

US Stock Futures Consolidate as Investors Await Jobless ClaimsStocks

-

Trump’s Davos Speech Sets the Tone as Markets Brace for Trade and Geopolitical RisksStocks

-

Markets Look to Data and Fed Rhetoric for DirectionStocks