U.S. Index Futures Pull Back Near Record Highs as Markets Await CPI

U.S. stock index futures move lower ahead of the Q4 earnings season, key CPI data and a potential Supreme Court ruling on tariffs.

Daniel Brooks

Daniel Brooks

Once again, investors are recalibrating expectations. U.S. stock index futures opened the week under pressure, with S&P 500 and Nasdaq futures edging lower as markets digest record highs and prepare for a dense macro and earnings calendar.

Market snapshot

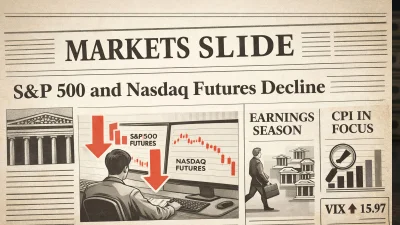

Previous session. The S&P 500 and Nasdaq closed the prior trading day higher. The S&P 500 posted a fresh all-time high, maintaining its position within a local uptrend. The Nasdaq Composite pushed through a short-term descending trendline and tested the 25,800 level.

Today. Futures on both indices are trading lower. S&P 500 futures remain above the 6,900 level, hovering close to record highs, with near-term support seen at 6,850. Nasdaq futures are trading below 25,900, sitting near the lower boundary of a local ascending channel. Key support is located around 25,500.

Key drivers this week

The primary focus is the start of the fourth-quarter earnings season, traditionally led by results from major U.S. banks. These reports are closely watched for signals on consumer credit, loan growth and net interest income trends.

In parallel, markets await the release of the December Consumer Price Index (CPI), which is expected to provide further clarity on the inflation trajectory and its implications for Federal Reserve policy.

Adding to uncertainty, investors are monitoring a potential U.S. Supreme Court decision on Trump-era tariffs, which could be announced as early as January 14 and may have implications for trade-sensitive sectors.

Recent labor market data showed the U.S. unemployment rate at 4.4% in December, slightly below market expectations, reinforcing the narrative of a still-resilient labor market.

On the rates front, the U.S. Treasury is scheduled to hold auctions of 3-year and 10-year notes later today, an event that could influence yields and broader risk sentiment.

Sector performance

Cyclical sectors showed mixed but generally positive performance. Aerospace & Defense, Materials and Consumer Discretionary were among the leaders, while Financials finished the session modestly lower.

Growth sectors largely advanced, led by Semiconductors and Technology. Cannabis and Solar-related segments underperformed.

Defensive sectors mostly moved higher, with Utilities leading gains, while Health Care ended slightly in negative territory.

Intermarket view

Crude oil prices tested the upper boundary of a medium-term descending channel and are trading near the $59 level.

U.S. Treasury yields continue to consolidate in a narrow range, holding below 4.2%.

The VIX volatility index is forming a gap higher toward the 16 level, approaching the upper boundary of a local ascending channel from December lows.

Gold has moved toward the upper boundary of its rising channel, briefly reaching the 4,600 level, highlighting persistent demand for defensive assets.

With valuations elevated and volatility stirring, early earnings results and inflation data may prove decisive for near-term direction.

-

S&P 500 and Nasdaq Futures Hold Steady as Markets Await Supreme Court RulingStocks

S&P 500 and Nasdaq Futures Hold Steady as Markets Await Supreme Court RulingStocks -

US Stock Futures Consolidate as Investors Await Jobless ClaimsStocks

-

S&P 500 and Nasdaq Futures Consolidate Near Record Highs as Volatility Stays SubduedStocks

-

S&P 500 and Nasdaq Futures Trade Sideways as PMI and Labor Data Take Center StageStocks

-

S&P 500 Futures Stabilize Above 6900 as Year-End Volumes ThinStocks

-

Wall Street Futures Pause Near Highs Ahead of US Housing and PMI DataStocks