More Than Half of US Debt to Be Rolled Over by 2028

More than half of US government debt must be refinanced between 2026 and 2028. With foreign central banks reducing Treasury exposure, markets are watching liquidity and Federal Reserve policy closely.

Olivia Carter

Olivia Carter

Between 2026 and 2028, the United States will need to refinance more than half of its outstanding federal debt — a refinancing wall that could shape liquidity conditions, bond yields, and Federal Reserve policy for years to come.

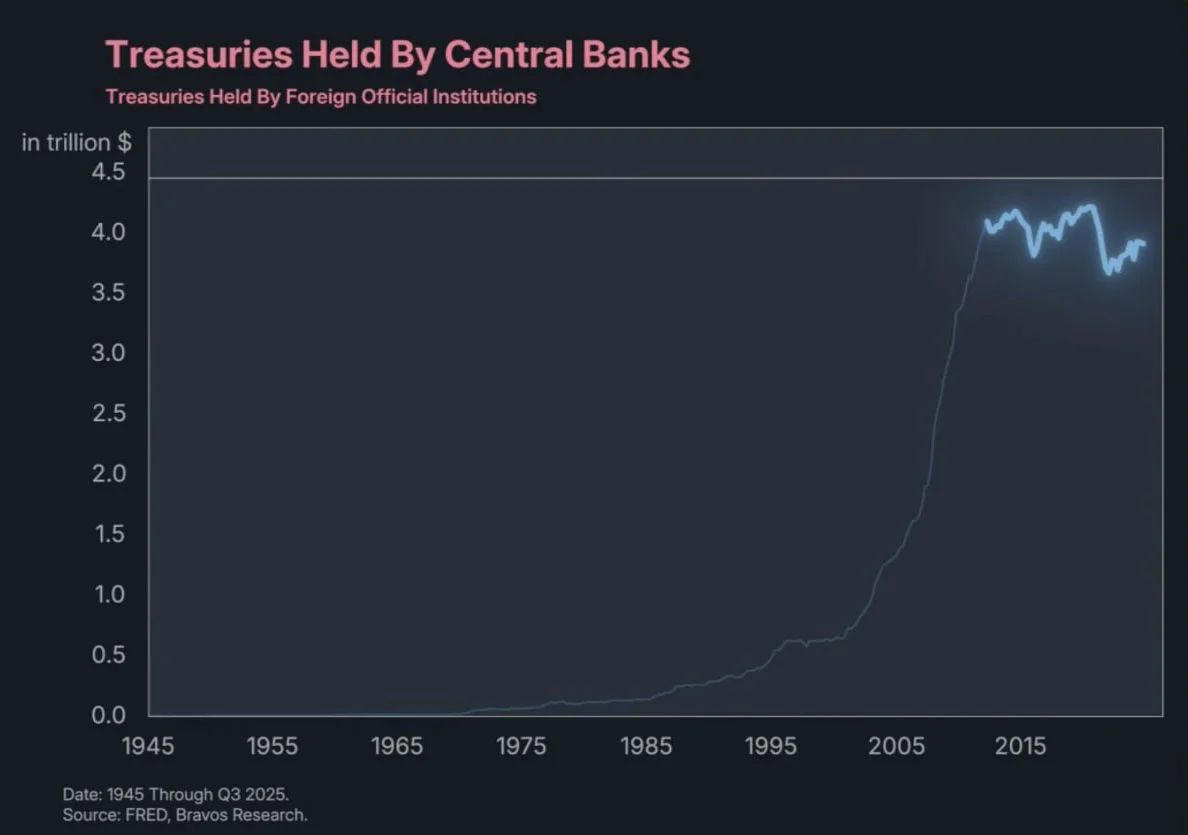

Foreign Central Banks Are No Longer Expanding Treasury Holdings

Data from FRED and Bravos Research show that foreign official institutions significantly increased Treasury holdings during the post-2008 era. However, that growth has plateaued — and in recent years, softened.

For over a decade, global central banks acted as a structural bid for US debt. That bid is no longer expanding at the same pace. In some cases, it is contracting.

This matters because the refinancing wave ahead is occurring in an environment where traditional external demand is less predictable than it was during the era of quantitative easing.

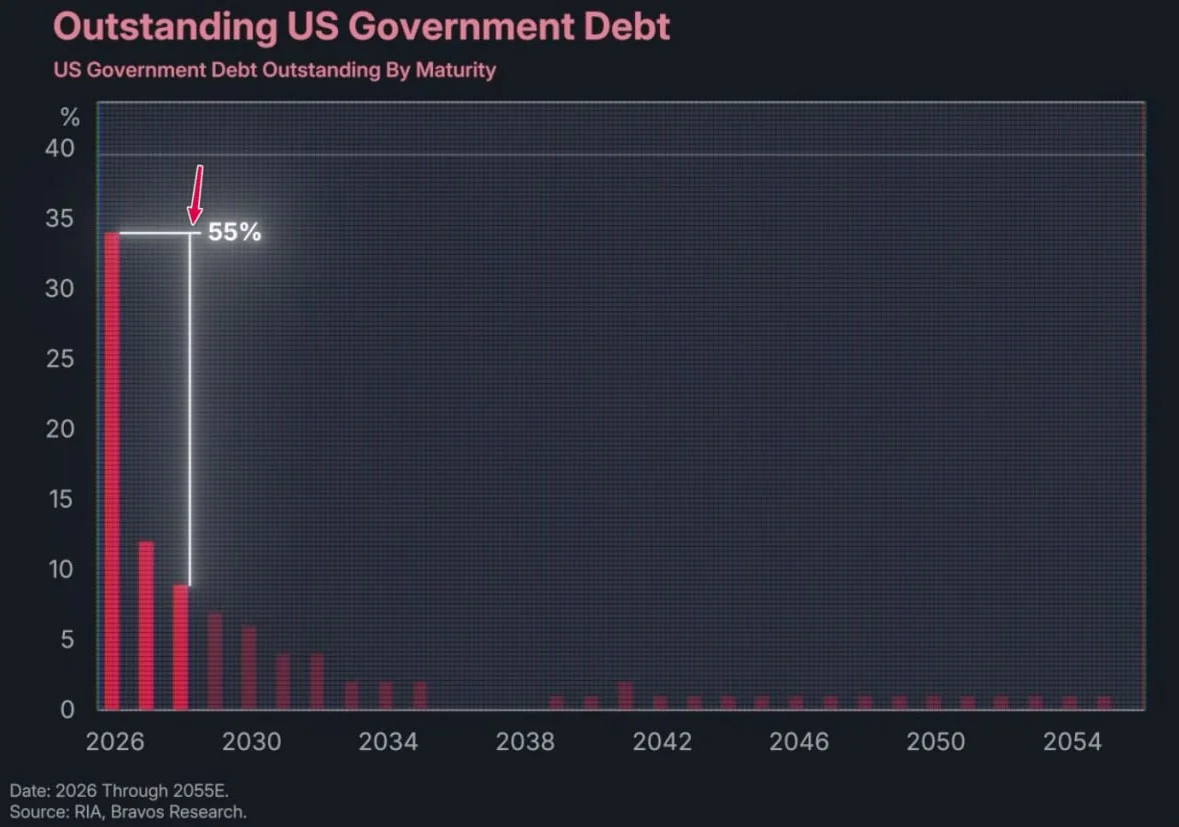

The Refinancing Wall: 2026–2028

According to maturity distribution estimates, more than 55% of US government debt outstanding will need to be refinanced between 2026 and 2028. The core issue is not simply the size — it is the rate environment.

Much of the debt issued during the 2010–2021 period carried historically low coupons. Refinancing into today’s higher-rate structure implies materially higher interest expenses unless yields decline meaningfully before rollover.

There are, broadly, two strategic paths available:

- Issue at higher yields — locking in elevated borrowing costs and increasing fiscal pressure.

- Rely more heavily on short-term Treasury bills while awaiting potential rate cuts.

The second strategy may provide flexibility, but it introduces rollover risk and amplifies liquidity sensitivity in money markets.

Liquidity Friction and the Fed Question

Such refinancing volumes help explain periodic episodes of what market participants describe as “liquidity friction.” When Treasury issuance rises sharply, it competes for capital across the financial system.

If foreign central banks are not expanding their holdings, domestic buyers — including US banks, asset managers, and potentially the Federal Reserve — must absorb the supply.

The Fed’s role becomes critical. While no formal commitment exists to expand its balance sheet, large-scale refinancing cycles historically coincide with shifts in monetary stance (as historical cycles often show).

Should financial conditions tighten excessively during the rollover period, markets may begin pricing in a more accommodative response.

Why Markets Are Watching Closely

Bond markets are forward-looking. The 2026–2028 maturity cluster is already influencing positioning across rates, dollar funding markets, and duration exposure.

Higher structural issuance can:

- Keep term premiums elevated.

- Increase volatility in long-duration Treasuries.

- Strengthen short-term funding demand.

- Pressure fiscal metrics through rising net interest costs.

In short, refinancing risk is not a distant concern — it is an evolving structural theme. The coming years will test whether the United States can smoothly navigate one of the largest debt rollover cycles in modern history without triggering sustained liquidity stress.

-

China’s Rising Debt and the Risk of a Financial Shock From the EastMacroeconomy

China’s Rising Debt and the Risk of a Financial Shock From the EastMacroeconomy -

Infrastructure Is Massively Undervalued Compared to Global Equities, BlackRock FindsMacroeconomy

-

Gold at 10,000 USD? Saxo Bank Lays Out Extreme “What If” Scenarios for 2026Macroeconomy

-

London Masks a Deep Economic Divide Inside the UKMacroeconomy

-

Musk: AI Could End the U.S. Debt Crisis in Three YearsMacroeconomy

-

US Data Center Investment Triples in Three Years as AI Drives Economic GrowthMacroeconomy